Author: Jamie Houston

Bristol Gate President and Chair of the Investment Committee, Mike Capombassis, was recently featured on BNN where he discussed ongoing tariff developments, how market concentration has progressed in 2025, as well as a few companies and areas of the market we are excited about.

Important Disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

In the November 27th issue of Value Investor Insights, Chief Investment Officer Izet Elmazi and Portfolio Manager Achilleas Taxildaris were interviewed and shared insights on the Bristol Gate investment process and highlighted two representative holdings, Broadcom and Old Dominion Freight Lines.

Article Highlights:

- Bristol Gate emphasizes a predictive approach to dividend growth, using machine learning to identify companies in the S&P 500 with strong earnings potential and sustainable competitive advantages. This forward-looking method distinguishes their strategy from traditional dividend investing by providing a focus list of the best predicted dividend growers over the next 12 months to the Fundamental team to select from.

- The concentrated 22-stock portfolio allows them to focus on high-quality businesses while confidently excluding those that don’t meet their rigorous standards for dividend growth, quality and valuation.

- Industries where capital discipline meets growth potential are a key focus. Their investments in areas like AI-driven semiconductors, less-than-truckload logistics, and enterprise software demonstrate this philosophy in action.

- Dividend growth serves as a reliable proxy for long-term earnings growth and shareholder returns. Bristol Gate’s strategy seeks to align with companies that signal confidence through reinvestment and increasing dividends.

Important disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

The information contained herein is obtained from multiple sources that are believed to be reliable. However, such information may not have been verified, and may be different from the information included in documents and materials created by a sponsor firm in whose investment program a client participates. Some sponsor firms may require that these Bristol Gate materials are preceded or accompanied by investment profiles or other documents or materials prepared by such sponsor firms, which will be provided upon a client’s request. There may be discrepancies between Bristol Gate’s performance returns and the returns included in a sponsor firm’s profile document (for example, but not limited to, differences in account size/type, portfolio management strategies, the number of securities held, average account size, inclusion of institutional or mutual fund accounts, etc.) For additional information, documents and/or materials, please speak to your Financial Advisor.

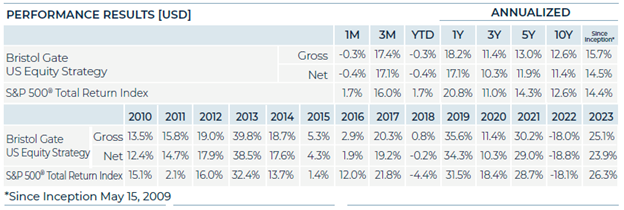

US Equity Strategy returns in this report refer to the Bristol Gate US Equity Strategy Composite (the “US Composite”). The US Composite consists of equities of publicly traded, dividend paying US companies. The US Composite is valued in US Dollars and for comparison purposes is measured against the S&P 500 Total Return Index. The US Composite’s Investment Advisor, Bristol Gate Capital Partners Inc., defines itself as a portfolio manager, exempt market dealer and investment fund manager (as per its registration in Ontario, its principal regulator in Canada) and is also a Registered Investment Adviser with the U.S. Securities and Exchange Commission (the “SEC”). The Investment Advisor’s objective is to select companies with positive dividend growth, and which collectively will generate over the long term a growing income and capital appreciation for investors. The inception date of the US Composite is May 15, 2009. The US Dollar is the currency used to measure performance, which is presented on a gross and net basis and includes the reinvestment of investment income. The US Composite’s gross return is gross of withholding tax prior to January 1, 2017 and is net of withholding tax thereafter. Net returns are calculated by reducing the gross returns by the maximum management fee charged by Bristol Gate of 1%, applied monthly. Actual investment advisory fees incurred by clients may vary. There is the opportunity for the use of leverage up to 30% of the net asset value of the underlying investments using a margin account at the prime broker. Thus far no material leverage has been utilized. An investor’s actual returns may be reduced by management fees, performance fees, and other operating expenses that may be incurred because of the management of the US Composite. A performance fee may also be charged on some accounts and funds managed by the firm. Bristol Gate claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To obtain a GIPS Composite Report, please email us at info@bristolgate.com.

The S&P 500® Total Return Index measures the performance of the broad US equity market, including dividend re-investment, in US dollars. This index is provided for information only and comparisons to the index has limitations. The benchmark is an appropriate standard against which the performance of the strategy can be measured over longer time periods as it represents the primary investment universe from which Bristol Gate selects securities. However, Bristol Gate’s portfolio construction process differs materially from that of the benchmark and the securities selected for inclusion in the strategy are not influenced by the composition of the benchmark. For example, the strategy is a concentrated portfolio of approximately equally weighted dividend-paying equity securities, rebalanced quarterly whereas the benchmark is a broad stock index (including both dividend and non-dividend paying equities) that is market capitalization weighted. As such, strategy performance deviations relative to the benchmark may be significant, particularly over shorter time periods. The strategy has concentrated investments in a limited number of companies; as a result, a change in one security’s value may have a more significant effect on the strategy’s value.

This Report is for information purposes and should not be construed under any circumstances as a public offering of securities in any jurisdiction in which an offer or solicitation is not authorized. Prospective investors in Bristol Gate’s pooled funds or ETF funds should rely solely on the fund’s offering documents, which outline the risk factors associated with a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax implications of any investment in a Bristol Gate fund.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, and it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events.

Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

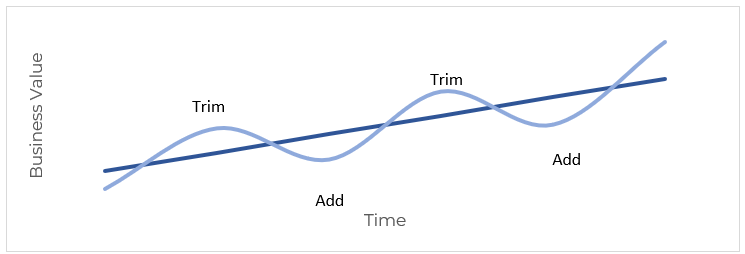

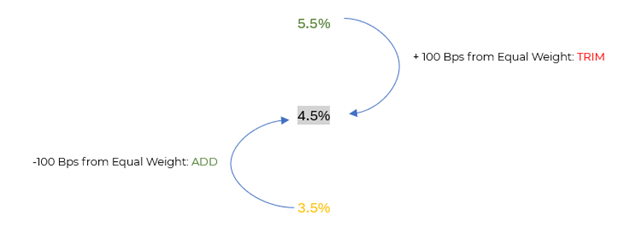

We are dedicated to identifying high-quality businesses with high prospective dividend growth. We aim to build resilient portfolios, which can withstand market volatility and deliver long-term returns. When it comes to portfolio construction, we spend considerable time thinking about the best way to manage an equally weighted portfolio outside of our regular re-balancing time periods. Our data science team has solved this issue by developing a methodical approach using stock price information to build a “threshold” framework which allows for stocks to rise and fall within certain pricing bands in the interim between re-balancing dates. This allows us to take advantage of the opportunities presented during short-term periods of market euphoria and fear.

As outlined in Exhibit 1, we have employed a strategic method to reallocate our investments to optimize portfolio performance. When the weight of any stock fluctuates more than 1% from its target equal weight of 4.55%, we automatically trim or add to those positions on a quarterly basis. As an example, a stock that has experienced gains and exceeds the threshold of 1% would be trimmed back to equal weight and in doing so capture profits and reinvest them into a portfolio company that the market may be undervaluing.

Exhibit 1: Bristol Gate Quarterly Rebalancing Approach

Source: Bristol Gate Capital Partners

We implemented this approach in 2021, based on our findings which examined its potential impact on performance. Our previous approach had been rebalancing all names that had deviated from their target weight, bringing the portfolio to equal weight on a quarterly basis. The results of our study determined that not only was there no detrimental impact on performance potential but that this approach to introduce thresholds would likely have a positive impact given the reduced trading costs associated with it.

From a process perspective, we believe this approach has two primary benefits. The first benefit is it acts as a contrarian system: it reduces our exposure to businesses with near-term valuations that may be stretched while simultaneously increasing our exposure to businesses trading at cheaper valuations. The second benefit is it demands conviction. If we are going to add to laggards which have become our smallest positions, we must discuss and determine the validity of our thesis with the investment committee. If the company’s poor performance is more likely a result of fundamental issues rather than short-term volatility, we are more likely to sell the name rather than add to it.

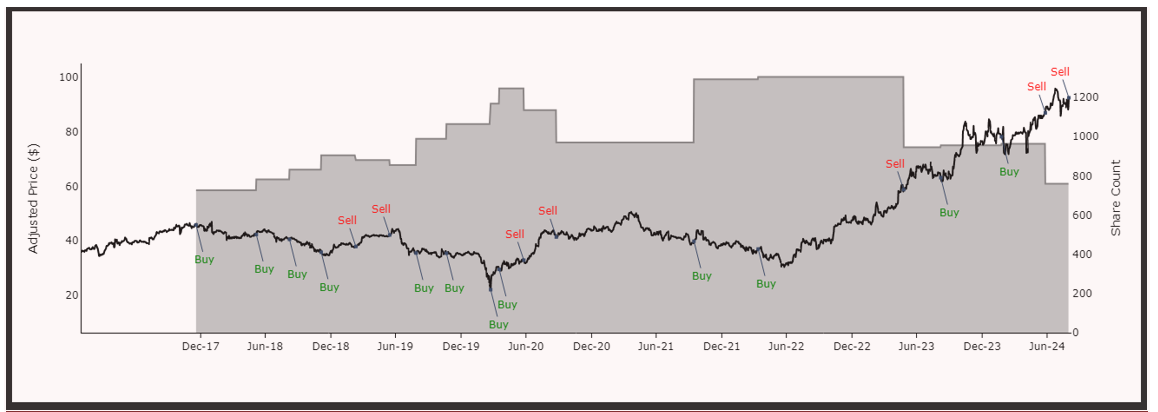

To demonstrate the impact of this rebalancing on the portfolio, we can look at the history of our ownership of Stella-Jones (SJ), one of the longest held names in our Bristol Gate Concentrated Canadian Equity ETF. SJ is a high-quality, high dividend grower that has fallen in and out of favour with the market since we first initiated our position in the company in 2017.

Throughout our ownership of Stella-Jones, our thesis has not changed. It is a market leader in two of its three main operating segments (utility poles and railway ties). It has discernible competitive advantages versus its competitors. Due to its scale, it can offer coast-to-coast service to large customers (such as Tier-1 Railways), as well as SJ’s treating facilities, which are both very hard to replicate. These advantages have allowed Stella-Jones to have a steady increase in sales volumes in both segments driven by maintenance demand. They also have pricing power, giving them the ability to pass on increasing input costs to their customers.

During the COVID pandemic in 2020, lumber prices shot up due to increased home improvement demand. This boosted Stella-Jones’ share price, and we were able to harvest gains twice during that period. Subsequently, as lumber demand normalized and prices fell after the pandemic, SJ’s revenue from its residential lumber segment fell too. Through our fundamental evaluation, we viewed the drop in share price as overly punitive and we were happy to add to the position.

Stella-Jones management’s medium-term guidance and positive quarterly results since mid-2023, driven by strong demand in utility poles due to increased infrastructure spending in the U.S., a large maintenance replacement cycle and an increase in environmental fires, have since helped its stock price reach new all-time highs. Once again allowing us to realize some profits by trimming our shares and reallocating to other under-appreciated names in our portfolio.

Exhibit 2 demonstrates the evolution of our investment in SJ since our initial investment. Stella-Jones’ stock price has gone from ~$45 to ~$92 between Dec 18, 2017 through August 31, 2024, resulting in a 102% cumulative return (or 11.1% annualized). Our rebalancing process has resulted in excess returns of 1.6% per year as opposed to if we had simply bought and held the stock.

Exhibit 2: Bristol Gate US Equity strategy ownership changes in Stella Jones

Source: Bloomberg, Bristol Gate Capital Partners

The key strength of a disciplined and rigorous investment process is its ability to provide consistency, irrespective of market conditions. At Bristol Gate, our investment strategy is firmly grounded in evidence-based methods, which helps us steer clear of emotional or reactionary decisions, regardless of what the market throws at us. This disciplined approach keeps us aligned with the long-term goals of our clients.

Performance Disclosure (As at August 31, 2024):

Important disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

Strategy returns in this report refer to the Bristol Gate Canadian Equity Strategy Composite (the “Composite”). The Composite consists primarily of equities of publicly traded, dividend paying Canadian companies. The Composite is valued in Canadian Dollars and for comparison purposes is measured against the S&P/TSX. The composite’s Investment Advisor, Bristol Gate Capital Partners Inc., defines itself as a portfolio manager, exempt market dealer and investment fund manager (as per its registration in Ontario, its principal regulator in Canada) and is also a Registered Investment Adviser with the U.S. Securities and Exchange Commission (the “SEC”). The Investment Advisor’s objective is to select companies primarily from the S&P/TSX universe with positive dividend growth and which collectively will generate over the long term a growing income and capital appreciation for investors. The inception date of the Composite is July 1, 2013. Returns are presented gross and net of fees and include the reinvestment of all income. The composite’s gross return is gross of withholding tax prior to January 1, 2017 and is net of withholding tax thereafter. Net returns are calculated by reducing the gross returns by the maximum management fee charged by Bristol Gate of 0.7%, applied monthly. Actual investment advisory fees incurred by clients may vary. An investor’s actual returns may be reduced by management fees, performance fees, and other operating expenses that may be incurred because of the management of the composite. A performance fee may be charged on some accounts and funds managed by the firm. Bristol Gate claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To obtain a GIPS Composite Report, please email us at info@bristolgate.com.

The S&P/TSX Total Return Index measures the performance of the broad Canadian equity market, including dividend re-investment, in Canadian dollars. This index is provided for information only and comparisons to the index have limitations. The benchmark is an appropriate standard against which the performance of the strategy can be measured over longer time periods as it represents the primary investment universe from which Bristol Gate selects securities. However, Bristol Gate’s portfolio construction process differs materially from that of the benchmark and the securities selected for inclusion in the strategy are not influenced by the composition of the benchmark. For example, the strategy is a concentrated portfolio of approximately equally weighted dividend-paying equity securities, rebalanced quarterly whereas the benchmark is a broad stock index (including both dividend and non-dividend paying equities) that is market capitalization weighted. As such, strategy performance deviations relative to the benchmark may be significant, particularly over shorter time periods. The strategy has concentrated investments in a limited number of companies; as a result, a change in one security’s value may have a more significant effect on the strategy’s value.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, and it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events.

Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

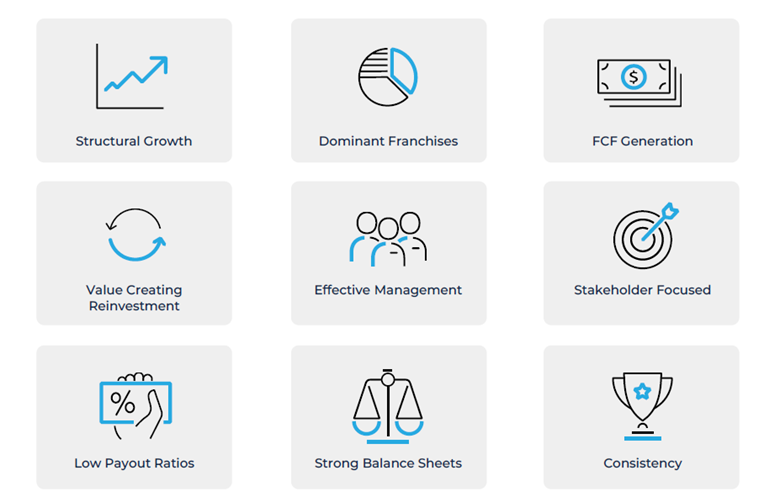

At Bristol Gate, we focus on investing in high-quality companies that demonstrate strong potential for high dividend growth. We utilize advanced machine learning algorithms alongside the assessment from our portfolio managers to help determine a company’s dividend growth and quality characteristics. Once we have determined a high level of confidence that a company will grow its dividend at a high rate, we look for specific traits that set these companies apart. What does a Bristol Gate company look like?

Structural Growth. Companies with strong pricing power and support from secular growth trends tend to exhibit structural growth. These companies can maintain a healthy level of growth over time, thanks to their ability to adapt to long-term market trends and sustain robust pricing strategies.

Dominant Franchises. We prefer companies that are dominant in their respective industries. Typically, these companies are a top three player in their space. This dominance can indicate a competitive advantage, ensuring they can sustain their market position and continue to grow.

Free Cash Flow (FCF) Generation. Companies that generate substantial free cash flow are able to meaningfully reinvest back into their business. While we focus on dividend growth, we like companies that allocate cash flow to high return investment opportunities as well. This reinvestment is crucial because it allows companies to earn high returns on invested capital. As equity owners, we want to see companies use their cash flow to fuel further growth and create additional value which will, in turn, drive future dividend growth.

Value Creating Reinvestment. High-quality companies have significant opportunities for value-creating reinvestment. These businesses can allocate capital effectively, reinvesting in areas that will generate high returns. This reinvestment strategy supports their long-term growth and enhances their overall value.

Effective Management. The best companies are led by management teams that excel at capital allocation. These teams know how to balance reinvestment in their own businesses, dividend growth, share buybacks, and strategic acquisitions to maximize shareholder value. Their ability to make smart capital allocation decisions is a key driver of their long-term success. Additionally, we appreciate when management compensation is aligned with shareholder interests and the long-term performance of the company.

Stakeholder Focused. Quality companies prioritize taking care of their customers, employees, and communities. A strong commitment to stakeholders not only ensures a positive impact on society but also contributes to the company’s sustainability and long-term success.

Low Payout Ratios. A lower payout ratio means the company retains more earnings, providing flexibility for future dividend growth. It also means the company sees significant value creation opportunities. A lower payout ratio often means dividend increases are sustainable over the long term.

Strong Balance Sheets. Financial strength is a non-negotiable trait for Bristol Gate companies. We only invest in companies whose debt is investment grade as rated by major rating agencies. A strong balance sheet ensures stability and reduces financial risk, making these companies more resilient during economic downturns.

Consistency. We value consistency and durability in businesses. Companies that demonstrate consistent performance and predictable results make it easier for us to forecast their future growth. This reliability allows us to sleep easier at night, knowing our investments are in stable, well-managed companies.

Our investment strategy focuses on high dividend growth companies. Within this group, we seek to identify and invest in companies that exhibit some or all of these “quality” traits. By doing so, we aim to build a portfolio of high-quality businesses poised for substantial dividend growth and long-term success.

Important Disclosures: There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements: This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

At Bristol Gate, we are specialists in High Dividend Growth investing – a unique subset in the dividend universe. We firmly believe our unique approach, which combines the power of machine learning with deep-rooted fundamental analysis, gives us an advantage.

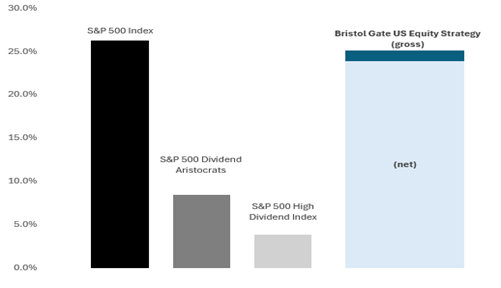

2023 was a strong year for our US Equity strategy as we outperformed our dividend-paying universe by a considerable margin (see Note 1). Looking forward, we believe there are robust return opportunities for the strategy, considering some of the current prevailing conditions:

- What does “passive” investing mean today?

Passive investing aims to provide investors with broad market exposure, based on the very simple logic that over time the market goes up. However, passively investing in the S&P 500 Index looks very different than how it has for most of its history.

Exhibit 1: S&P 500 Index Concentration and Earnings Contribution since 1996

Source: JPMorgan Guide to the Markets, Jan 31, 2024.

The S&P 500 Index today seems to have more in common with how it was constructed during the tech bubble and global financial crisis. Both the index’s concentration and the contribution to the total earnings of the index by its largest constituents are reflective of those periods. In both these past scenarios, market concentration was alleviated by sharp market drawdowns.

Although we are concentrated investors, we believe diversification needs to be mindful and having our largest weights determined by past performance does not seem prudent to us.

- Valuation matters

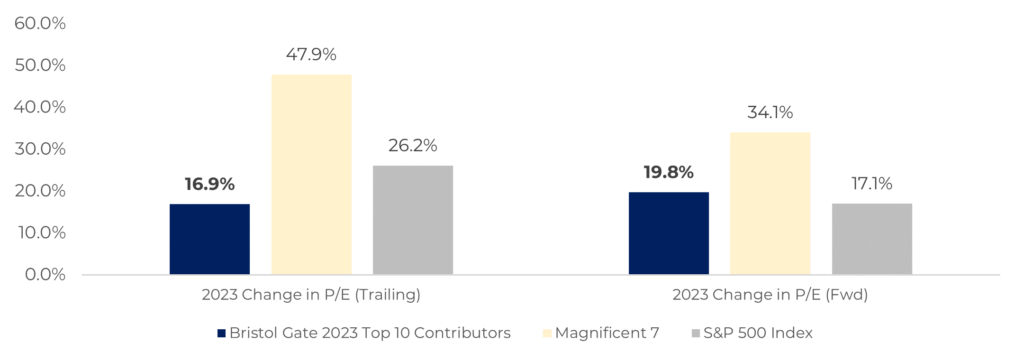

The Magnificent 7’s outsized weight in the S&P 500 also has an impact on the valuation for the broad market. That subset of stocks contributed over 60% of the Index’s total return in 2023. When compared with the top 10 contributors to our US Equity strategy’s returns, we can see how their valuation changed relative to our best performing names last year:

Exhibit 2: % Change in Valuation of Bristol Gate US Equity Strategy Top 10 Contributors, S&P 500 Index & Magnificent 7 in 2023

Source: Bristol Gate Capital Partners, Bloomberg. As of December 31, 2023

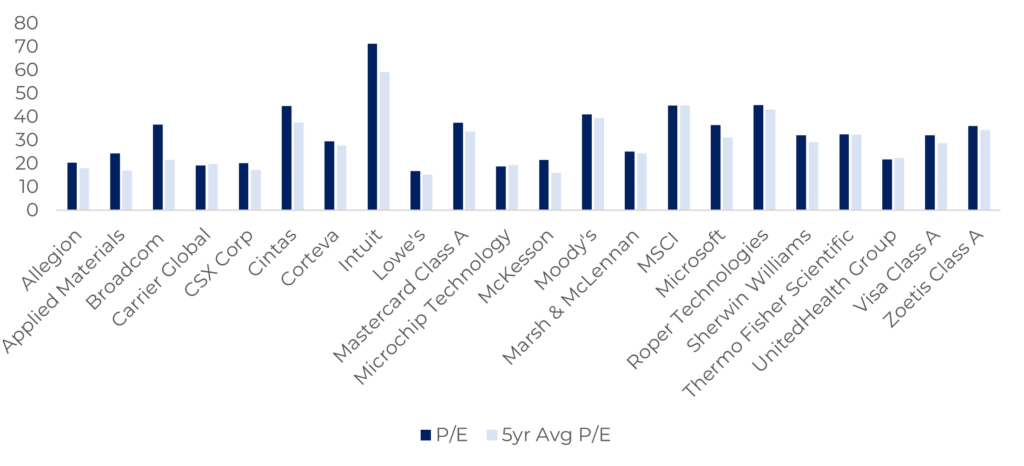

In fact, most of our portfolio companies are not trading at widely divergent levels relative to their 5-year average valuations:

Exhibit 3: % Current vs 5 Year Average P/E (Trailing) of Bristol Gate US Equity Strategy

Source: Bristol Gate Capital Partners, Bloomberg. As at Feb 16, 2024

As bottom-up investors, we are more comfortable with the valuations of the 22 stocks in our US Equity portfolio rather than those of the stocks that currently constitute the largest weights of the index, and as a result, will likely have a large impact on its returns.

- Our portfolio is constructed for all market environments.

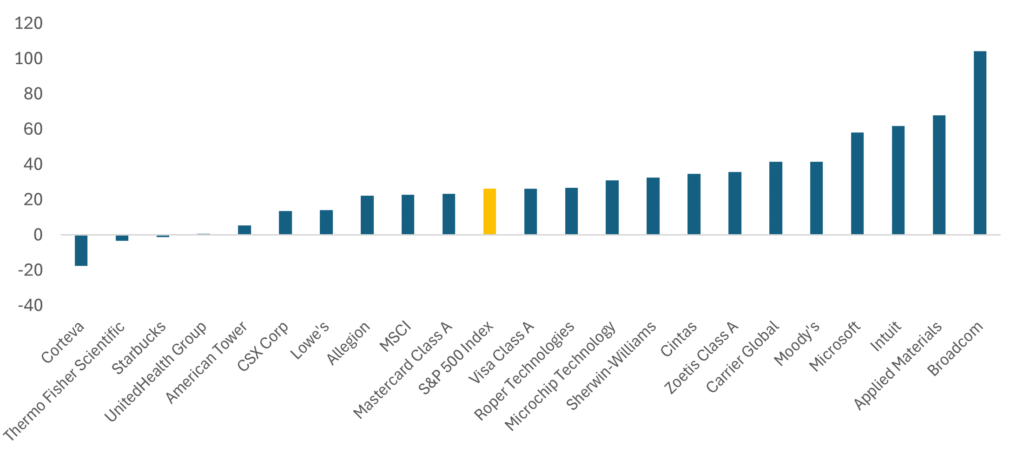

Our goal is to build a diversified portfolio, which means not all the companies will move in lockstep. These companies have different exposures that account for different risks at different times in a market cycle. By design, we expect our portfolio to have laggards in any given year as a result, and last year was no different:

Exhibit 4: Bristol Gate US Equity Strategy Holdings: 2023 Stock Total Return vs S&P 500 Index Total Return (%)

Source: Bristol Gate Capital Partners, Bloomberg. As of December 31, 2023

In the short term, we can not control what the price of a stock will do. It is affected by any number of reasons including macroeconomics, industry or company specific issues or even just sentiment. However, by focusing on what we can control and investing in companies with strong dividend growth prospects supported by high quality fundamentals, it becomes easier to withstand these fluctuations.

Our rebalancing approach seeks to take advantage of periods of market euphoria and fear. On rebalancing dates, we add to positions that fall below a predefined threshold and subtract from positions that rise above a higher threshold. By following this contrarian process, we seek to reduce valuation risk while trying to maximize the potential internal rate of return of our portfolio over time.

Bristol Gate Systematic, Contrarian Rebalancing Approach

For Illustrative Purposes Only. Source: Bristol Gate Capital Partners.

We are diligently focused on seeking out high quality companies that are growing their dividends at high rates, ensuring we pay a fair price for them. Our conviction in our unique approach and disciplined process supports our belief that our clients will benefit over the long-term.

Note 1: 2023 Returns.

Source: Bristol Gate Capital Partners, Morningstar Direct.

Performance Disclosure (As at January 31, 2024):

Important Disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

US Equity Strategy returns in this report refer to the Bristol Gate US Equity Strategy Composite (the “Composite”). The Composite consists of equities of publicly traded, dividend paying US companies. The Composite is valued in US Dollars and for comparison purposes is measured against the S&P 500 Total Return Index. The composite’s Investment Advisor, Bristol Gate Capital Partners Inc., defines itself as a portfolio manager, exempt market dealer and investment fund manager (as per its registration in Ontario, its principal regulator in Canada) and is also a Registered Investment Adviser with the U.S. Securities and Exchange Commission (the “SEC”). The Investment Advisor’s objective is to select companies with positive dividend growth, and which collectively will generate over the long term a growing income and capital appreciation for investors. The inception date of the Composite is May 15, 2009. The US Dollar is the currency used to measure performance, which is presented on a gross and net basis and includes the reinvestment of investment income. The composite’s gross return is gross of withholding tax prior to January 1, 2017 and is net of withholding tax thereafter. Net returns are calculated by reducing the gross returns by the maximum management fee charged by Bristol Gate of 1%, applied monthly. Actual investment advisory fees incurred by clients may vary. There is the opportunity for the use of leverage up to 30% of the net asset value of the underlying investments using a margin account at the prime broker. Thus far no material leverage has been utilized. An investor’s actual returns may be reduced by management fees, performance fees, and other operating expenses that may be incurred because of the management of the composite. A performance fee may also be charged on some accounts and funds managed by the firm. Bristol Gate claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. To obtain a GIPS Composite Report, please email us at info@bristolgate.com.

The S&P 500® Total Return Index measures the performance of the broad US equity market, including dividend re-investment, in US dollars. This index is provided for information only and comparisons to the index has limitations. The benchmark is an appropriate standard against which the performance of the strategy can be measured over longer time periods as it represents the primary investment universe from which Bristol Gate selects securities. However, Bristol Gate’s portfolio construction process differs materially from that of the benchmark and the securities selected for inclusion in the strategy are not influenced by the composition of the benchmark. For example, the strategy is a concentrated portfolio of approximately equally weighted dividend-paying equity securities, rebalanced quarterly whereas the benchmark is a broad stock index (including both dividend and non-dividend paying equities) that is market capitalization weighted. As such, strategy performance deviations relative to the benchmark may be significant, particularly over shorter time periods. The strategy has concentrated investments in a limited number of companies; as a result, a change in one security’s value may have a more significant effect on the strategy’s value.

S&P 500 ® Total Return Dividend Aristocrats Index measures the performance of a subset of S&P 500® Index companies that have increased their dividends every year for the last 25 consecutive years. This Index has limited relevancy to our approach as it focuses on historical dividend growth, whereas Bristol Gate’s US Equity strategy’s securities are selected based on future dividend growth.

S&P 500 ® High Dividend Index is designed to measure the performance of 80 high yield companies within the S&P 500 and is equally weighted to best represent the performance of this group, regardless of constituent size. This Index has limited relevancy to our approach as it focuses on dividend yield, whereas Bristol Gate’s US Equity strategy’s securities are selected based on future dividend growth.

SPDR® S&P 500® ETF Trust (SPY US) sourced from Bloomberg has been used as a proxy for the S&P 500® Total Return Index for the purpose of providing non-return-based portfolio statistics and sector weightings in this report. SPY US is an ETF that seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the S&P 500® Index.

This Report is for information purposes and should not be construed under any circumstances as a public offering of securities in any jurisdiction in which an offer or solicitation is not authorized. Prospective investors in Bristol Gate’s pooled funds or ETF funds should rely solely on the fund’s offering documents, which outline the risk factors associated with a decision to invest. No representations or warranties of any kind are intended or should be inferred with respect to the economic return or the tax implications of any investment in a Bristol Gate fund.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, and it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events.

Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

Artificial Intelligence (AI) is no longer a concept confined to science fiction or high-tech laboratories. This past year, AI has reached consumers in ways previously unimagined. The rise of Large Language Models (LLMs), such as ChatGPT, has given people an entirely new way of approaching problems. Engineers are using LLMs to help them write code, writers to help improve their flow, academics to summarize research papers, and the list goes on. The number of industries touched by this technology is quite remarkable. This raises the question: How will the rise of LLMs affect wealth managers?

At Bristol Gate, we have been incorporating AI into our process from the beginning. We are committed to staying at the forefront of technology through a process of continuous improvement and analysis of new technologies. Our history of combining man and machine has taught us how to implement technology to its full capabilities while not blindly putting faith into a black box algorithm. Our data science team has a long, successful track record of accurately predicting a company’s future dividend growth. These predictions inform our investment process and allow our portfolio managers to make unbiased, data-driven decisions that result in long-term wealth creation for our clients. We have always been strong believers in the synergies between AI and human intelligence and believe that many businesses can benefit from the integration of technology into their practices.

What LLMs Are Not

When talking about the potential of LLMs, it is important to first recognize what they are not. Large Language Models are not the golden solution that can be set off with no forethought and be expected to produce good results. In their current state, LLMs are most effectively used when combined with human insight. A good analogy for this relationship is a pilot and autopilot. Consider the human as the pilot and the AI as the autopilot; the pilot must determine the course of the flight and engage the autopilot appropriately, ensuring the flight stays on track and meets its objectives. Just as the pilot doesn’t rely solely on the autopilot for all decisions, effective use of LLMs requires human oversight to guide and utilize their capabilities for meaningful outcomes.

There are many known limitations that these models have and one of the major considerations that users should be aware of is when a model “hallucinates”. A hallucination is when a generative model produces incorrect information and presents it as true. For example, if you were to ask ChatGPT about specific compliance rules for investment advisors, the output may include false information that could harm your practice should you blindly trust the response. For this reason, the best use cases of these models are when they complement human expertise rather than replace it. They should not be used and trusted as the sole source of information for critical decision-making processes and the answers should always be cross-referenced with trusted sources to ensure accuracy.

Another concern with LLMs is the issue of bias in training data. These models are trained on very large datasets, which inevitably include biased or skewed perspectives. This can lead to outputs that unintentionally perpetuate these biases, whether related to political stances, opinions on the economy, or other factors. While LLMs can process and synthesize information at a remarkable scale, they do so based on the data they have been trained on, which may not always be neutral or comprehensive. This once again highlights the need for a balanced approach where human oversight is used to identify and mitigate these biases.

Use Cases

Knowing that we cannot expect ChatGPT to autonomously run a firm’s marketing, or take over the role of the CFO, there are many different areas which we can focus on that ChatGPT can help with.

Brainstorming. ChatGPT does a fantastic job of helping humans organize their thoughts and providing useful suggestions for further development. A simple query such as, ‘Please give me blog post ideas on taxes and investors’, can offer advisors a range of content ideas. For blog posts, it might not be smart to have ChatGPT write the whole thing, but continuing the conversation and asking ChatGPT to develop the structure of the blog can also be very helpful.

Learning and exploring. For simple topics, ChatGPT can be an excellent tutor. Generative AI models are great at simplifying information and presenting it in a style that works for you. Asking the model to explain something like a typical risk management process can be a great learning tool, especially when follow up questions are asked by the user to help with understanding. Follow-up questions are particularly important as they give users the ability to ask a near unlimited number of questions to refine their understanding. For example, after asking ChatGPT about a typical risk management process, a good follow-up question could be, ‘Can you explain how stress testing fits into this process?’. This back-and-forth conversation is very helpful when breaking down larger or more complex topics.

Text analysis. ChatGPT does an excellent job at traditional Natural Language Processing tasks such as summarization, extracting entities, or judging sentiment. By passing long or complex texts to ChatGPT with a specific task of summarizing in a specific tone, or extracting all company names, or even judging sentiment on a scale of 1 through 10, users can quickly absorb information that would have otherwise taken a larger amount of time.

Social Media. While the cases of brainstorming and idea generation have already been touched on, there are other, unique ways to utilize this technology. If you have previously written content, either on your company website, your pitch deck, or even blog posts, you can pass these documents to ChatGPT and ask to generate social media posts based off those topics. This is a handy way of repurposing content that you have already created.

Creative writing. Another valuable use case for wealth managers is leveraging ChatGPT’s creative writing ability. ChatGPT has the great ability to make complex topics seem simple and can help with your firm’s communications to clients. For example, if you have a highly technical report and would like to quickly communicate the insights to non-technical clients, ChatGPT can help you transform your report into one that is digestible by a wider audience.

Final Remarks

The rise of LLMs offers promising avenues for various aspects of practice management for wealth managers. While not a perfect solution to all of our problems, these AI tools can significantly aid in areas such as brainstorming, learning, analysis, and marketing. As long as we are aware of the shortcomings of these models and exercise caution and good judgement, LLMs can provide users with incredible use cases that can save time and increase output. If you are ever short on ideas of how LLMs can help your practice, it can help to ask yourself the question, what would I do if I had the power of 5,000 10th graders on my team?

Important Disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

Takes 2 minutes

Takes 2 minutes