Author: admin

FOR IMMEDIATE RELEASE

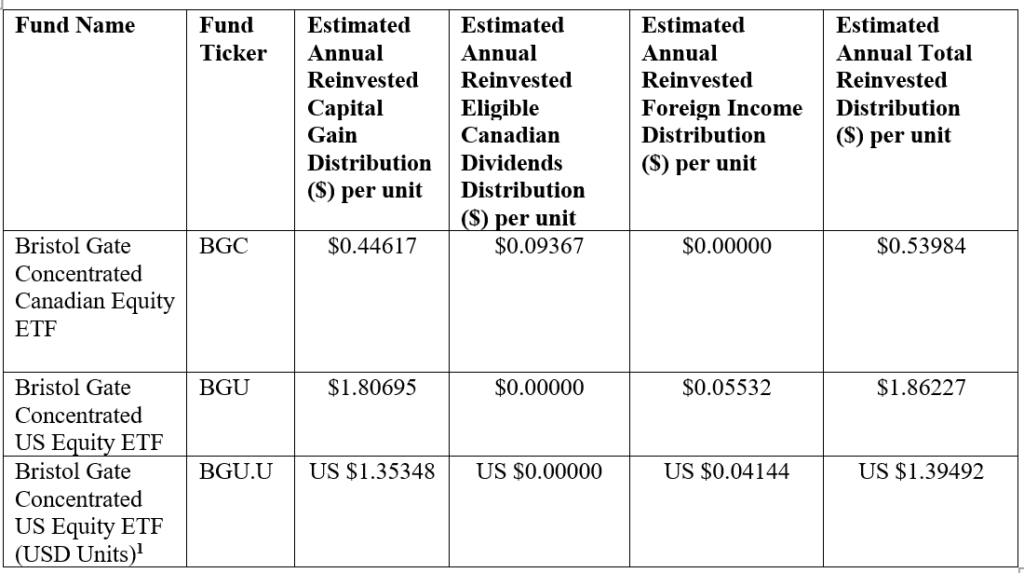

TORONTO, January 19, 2023 /CNW/ – Bristol Gate Capital Partners Inc. (“Bristol Gate Capital Partners” or the “firm”) today announced the final annual 2022 reinvested distributions for the Bristol Gate Exchange-Traded Funds (the “Bristol Gate ETFs”).

Unitholders of record on December 30, 2022 received notional distributions representing net investment income and/or realized capital gains within the Bristol Gate ETFs for the 2022 taxation year. A notional distribution is when the units from a reinvested distribution are immediately consolidated with the units held prior to the distribution and the number of units held after the distribution is identical to the number of units held before the distribution.

The taxable amounts of reinvested distributions for 2022, including tax characteristics of the distributions, will be reported to brokers through Clearing and Depository Services (CDS) within the first 60 days

of 2023. All values are expressed in Canadian dollars, unless otherwise indicated. This information is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for providing such advice.

Details of the per-unit reinvested distributions for the Bristol Gate ETFs are as follows:

| Fund Name | Fund Ticker | Annual Reinvested Capital Gain Distribution ($) per unit | Annual Reinvested Eligible Canadian Dividends Distribution ($) per unit | Annual Reinvested Foreign Income Distribution ($) per unit | Annual Total Reinvested Distribution ($) per unit |

| Bristol Gate Concentrated Canadian Equity ETF | BGC | $1.71901 | $0.18994 | $0.00000 | $1.90895 |

| Bristol Gate Concentrated US Equity ETF | BGU | $1.82477 | $0.00000 | $0.08230 | $1.90707 |

| Bristol Gate Concentrated US Equity ETF (USD Units)1 | BGU.U | US $1.34674 | US $0.00000 | US $0.06074 | US $1.40748 |

1Distribution per unit amount is reported in USD for BGU.U converted as at December 30, 2022

Commissions, management fees and expenses all may be associated with investments in exchange-traded funds (ETFs). Before investing, investors should carefully read the prospectus and ETF facts and carefully consider the investment objectives, risks, charges and expenses of the ETFs. ETFs are not guaranteed; their values change frequently, and past performance may not be repeated. For this and more complete information about the Bristol Gate ETFs call 416-921-7076 or visit www.bristolgate.com for the prospectus and ETF facts. Copies of the prospectus and ETF facts are also available on www.sedar.com.

About Bristol Gate Capital Partners Inc.

Bristol Gate Capital Partners is an independent, employee-owned, Toronto-based investment management company serving individual and institutional clients. The firm uses predictive machine learning in combination with fundamental analysis to identify high quality companies that have the capacity and willingness to significantly increase their dividends in the year ahead. Bristol Gate Capital Partners currently manages $2.6 billion in AUM/AUA across a US equity strategy and a Canadian equity strategy and manages an ETF following each strategy. To learn more information, please visit www.bristolgate.com.

For more information, please contact:

Michael Capombassis

President

416-921-7076 x 248

mike.capombassis@bristolgate.com

Important Disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

Though inflation and rising rates have dominated the headlines this year, it was not that long ago that investors were scrambling for income through a decade of low interest rates. Realizing the appetite for yield, many companies increased their dividend by any means necessary, hoping to become attractive income options for investors.

One such company is Algonquin Power & Utilities Corp (AQN), of which the Globe & Mail recently declared, “Algonquin’s days as a dividend growth darling are over.”

While on the surface AQN seemed to be the ideal company for our approach, we sold it from our Canadian high dividend growth strategy in 2018 (ETF ticker: BGC). We believe the sale highlighted how Bristol Gate’s integrated human + machine approach led to a better long-term outcome for investors.

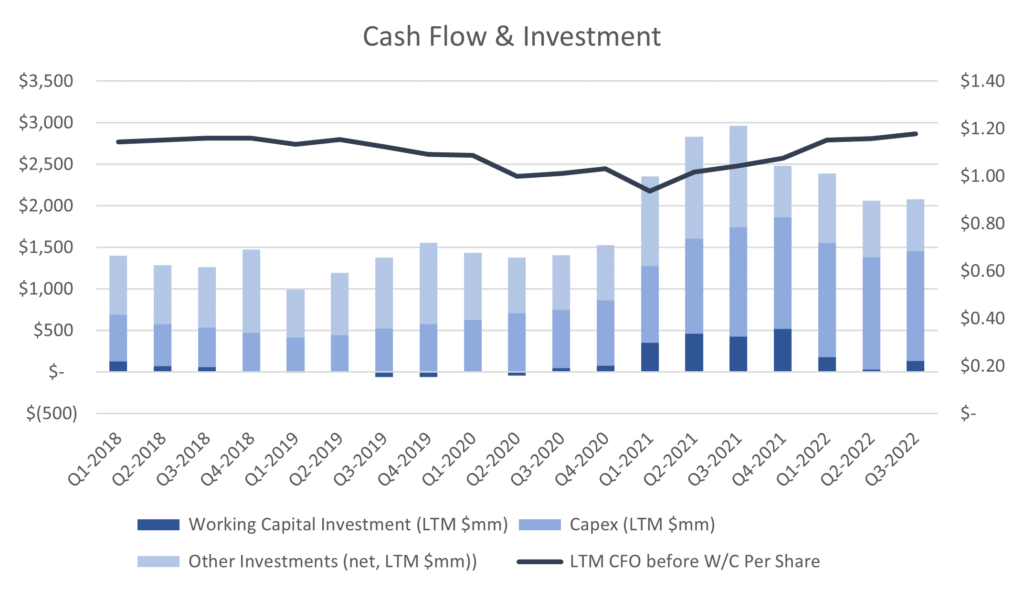

At the time of sale, our dividend growth prediction model continued to forecast attractive dividend growth for the company. Yet, our portfolio managers became concerned about several trends: operating cash flow per share was stagnant despite significant investment in the business and the company needed the capital markets to finance that investment.

Exhibit 1: Algonquin Operating Metrics

Source: Bristol Gate Capital Partners, Canalyst, FactSet

These characteristics were not consistent with those we seek in our investments and our portfolio managers concluded the dividend growth was not sustainable.

After we sold the shares, Algonquin continued to grow its dividend (8.9% compound annual growth rate from 2018-2022) and its shares performed well as the renewable energy sector took off. However, the trends our portfolio managers had identified continued and the company’s payout ratio increased substantially along with its leverage.

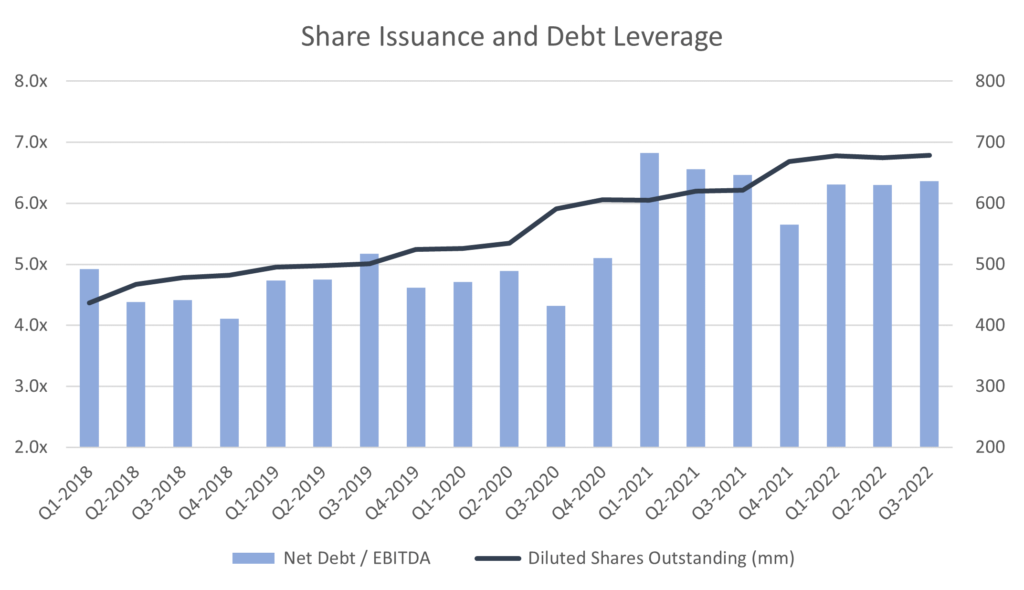

We avoid companies with poor returns on investment and a reliance on capital markets to continually fund their business models. Today, market turbulence has raised the cost of issuing debt or equity to prohibitive levels for many companies, including AQN.

Since 2020, our machine learning model’s predictions for the company’s dividend growth have been on a downward trend. By the end of September this year, our predictions had become markedly negative, confirming our team’s fundamental work.

Exhibit 2: Algonquin Power & Utilities Corp. Dividend Prediction History

Source: Bristol Gate Capital Partners, FactSet

Bristol Gate’s investment strategy is built on buying businesses that are poised to substantially grow their dividend over the next 12 months and beyond. Where many dividend investing strategies focus on a security’s dividend yield today, we have our eyes firmly on what lies beyond the horizon. We think our process and focus on sustainable dividend growth is a more sustainable investment strategy that ultimately leads to attractive long-term returns for our clients and partners.

Important Disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

For Immediate Release

TORONTO, November 23, 2022 /CNW/ – Bristol Gate Capital Partners Inc. (“Bristol Gate Capital Partners” or the “firm”) today announced the estimated 2022 reinvested distributions for the Bristol Gate Exchange-Traded Funds (the “Bristol Gate ETFs”). These annual reinvested distributions generally represent realized capital gains and/or excess net income within the Bristol Gate ETFs.

The distributions will not be paid in cash but will be reinvested and reported as a taxable distribution. The reinvested distributions will increase the unitholder’s adjusted cost base for the respective ETF. The ex-dividend date for the 2022 annual distributions will be December 29, 2022. Unitholders of record on December 30, 2022 will receive the actual 2022 reinvested distributions which may vary from the estimated amounts disclosed below.

Note that these figures are estimates only, as of November 17, 2022, are not guaranteed and are subject to change prior to the December 31, 2022 taxation year-end of the ETFs.

The actual taxable amounts of reinvested distributions for 2022, including the tax characteristics of the distributions, will be reported to brokers through Clearing and Depository Services (CDS) in early 2023.

All values are expressed in Canadian dollars, unless otherwise indicated. The estimated 2022 annual per-unit reinvested distributions for the Bristol Gate ETFs are as follows:

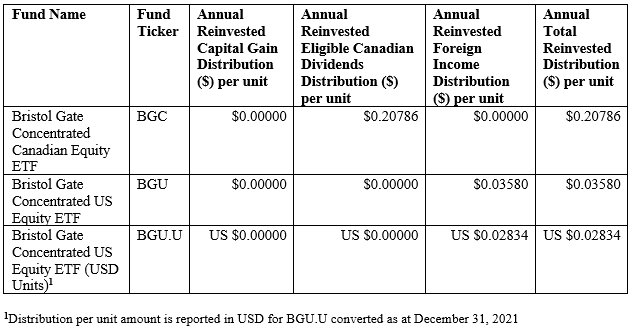

1Distribution per unit ($) amount is reported in USD for BGU.U converted as at November 17, 2022

Important Disclosures

Certain statements in this document may contain forward-looking statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks and uncertainties, including the risks described in the Prospectus of the ETF, uncertainties and assumptions about the ETF, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events.

Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements made by the ETF. The Manager has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

Commissions, management fees and expenses all may be associated with investments in exchange-traded funds (ETFs). Before investing, investors should carefully read the prospectus and ETF facts and carefully consider the investment objectives, risks, charges and expenses of the ETFs. ETFs are not guaranteed; their values change frequently, and past performance may not be repeated. For this and more complete information about the ETFs call 416-921-7076 or visit www.bristolgate.com for the prospectus and ETF facts. Copies of the prospectus and ETF facts are also available on www.sedar.com.

About Bristol Gate Capital Partners Inc.

Bristol Gate Capital Partners is an independent, employee-owned, Toronto-based investment management company serving individual and institutional clients. The firm uses predictive machine learning in combination with fundamental analysis to identify high quality companies that have the capacity and willingness to significantly increase their dividends in the year ahead. Bristol Gate Capital Partners currently manages approximately $2.6 billion in AUM/AUA across a US equity strategy and a Canadian equity strategy and manages an ETF following each strategy. To learn more information, please visit www.bristolgate.com.

For more information, please contact:

Michael Capombassis

President

416-921-7076 x 248

mike.capombassis@bristolgate.com

Important Disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

Bristol Gate Capital Partners CIO, Izet Elmazi, discusses the current inflationary environment and its impact on our portfolios.

Important Disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

For Immediate Release

Bristol Gate Capital Partners Inc. Announces Lead Portfolio Manager of Bristol Gate Concentrated Canadian Equity ETF

TORONTO, February 28, 2022 /CNW/ – Bristol Gate Capital Partners Inc. (“Bristol Gate” or the “firm”), announced a change to the lead portfolio manager of Bristol Gate Concentrated Canadian Equity ETF. Bristol Gate is the manager of Bristol Gate Concentrated Canadian Equity ETF (TSX: BGC) and Bristol Gate Concentrated US Equity ETF (TSX: BGU/BGU.U) (the “Bristol Gate ETFs”).

Investment decisions for each Bristol Gate ETF are made by a portfolio management team that has a lead portfolio manager and are subject to oversight by Bristol Gate’s Investment Committee. The firm announced that, effective February 28, 2022, Achilleas Taxildaris, Portfolio Manager, is the lead portfolio manager for Bristol Gate Concentrated Canadian Equity ETF. Mr. Taxildaris remains part of the portfolio management team for Bristol Gate Concentrated US Equity ETF. Izet Elmazi, Chief Investment Officer, continues as the lead portfolio manager for Bristol Gate Concentrated US Equity ETF and remains part of the portfolio management team for Bristol Gate Concentrated Canadian Equity ETF.

About Bristol Gate

Bristol Gate is an independent, employee-owned, Toronto-based investment management company serving individual and institutional clients. The firm uses predictive machine learning in combination with fundamental analysis to identify high quality companies that have the capacity and willingness to significantly increase their dividends in the year ahead. Bristol Gate currently manages approximately $2.9 billion in AUM/AUA across a US equity strategy and a Canadian equity strategy and manages an ETF following each strategy. To learn more information, please visit www.bristolgate.com.

For more information, please contact:

Michael Capombassis

President

416-921-7076 x 248

mike.capombassis@bristolgate.com

Important Disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

FOR IMMEDIATE RELEASE

TORONTO, January 12, 2022 /CNW/ – Bristol Gate Capital Partners Inc. (“Bristol Gate Capital Partners” or the “firm”) today announced the final annual 2021 reinvested distributions for the Bristol Gate Exchange-Traded Funds (the “Bristol Gate ETFs”).

Unitholders of record on December 31, 2021 received notional distributions representing net investment income and/or realized capital gains within the ETFs for the 2021 taxation year. A notional distribution is when the units from a reinvested distribution are immediately consolidated with the units held prior to the distribution and the number of units held after the distribution is identical to the number of units held before the distribution.

The taxable amounts of reinvested distributions for 2021, including tax characteristics of the distributions, will be reported to brokers through Clearing and Depository Services (CDS) within the first 60 days

of 2022. All values are expressed in Canadian dollars, unless otherwise indicated. This information is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for providing such advice.

Details of the per-unit reinvested distributions for the Bristol Gate ETFs are as follows:

Commissions, management fees and expenses all may be associated with investments in exchange-traded funds (ETFs). Before investing, investors should carefully read the prospectus and ETF facts and carefully consider the investment objectives, risks, charges and expenses of the ETFs. ETFs are not guaranteed; their values change frequently, and past performance may not be repeated. For this and more complete information about the ETFs call 416-921-7076 or visit www.bristolgate.com for the prospectus and ETF facts. Copies of the prospectus and ETF facts are also available on www.sedar.com.

Important Disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

For more information, please contact:

Michael Capombassis

President

416-921-7076 x 248

FOR IMMEDIATE RELEASE

TORONTO, November 19, 2021 /CNW/ – Bristol Gate Capital Partners Inc. (“Bristol Gate Capital Partners” or the “firm”) today announced the estimated 2021 reinvested distributions for the Bristol Gate Exchange-Traded Funds (the “Bristol Gate ETFs”). These annual reinvested distributions generally represent realized capital gains and/or excess net income within the Bristol Gate ETFs.

The distributions will not be paid in cash but will be reinvested and reported as a taxable distribution. The reinvested distributions will increase the unitholder’s adjusted cost base for the respective ETF. The ex-dividend date for the 2021 annual distributions will be December 30, 2021. Unitholders of record on December 31, 2021 will receive the actual 2021 reinvested distributions which may vary from the estimated amounts disclosed below.

Note that these figures are estimates only, as of November 15, 2021, are not guaranteed and are subject to change prior to the December 31, 2021 taxation year-end of the ETFs.

The actual taxable amounts of reinvested distributions for 2021, including the tax characteristics of the distributions, will be reported to brokers through Clearing and Depository Services (CDS) in early 2022.

All values are expressed in Canadian dollars, unless otherwise indicated. The estimated 2021 annual per-unit reinvested distributions for the Bristol Gate ETFs are as follows:

Important Disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

About Bristol Gate Capital Partners Inc.

Bristol Gate Capital Partners is an independent, employee-owned, Toronto-based investment management company serving individual and institutional clients. The firm uses predictive machine learning in combination with fundamental analysis to identify high quality companies that have the capacity and willingness to significantly increase their dividends in the year ahead. Bristol Gate Capital Partners currently manages approximately $2.8 billion in AUM/AUA across a US equity strategy and a Canadian equity strategy and manages an ETF following each strategy. To learn more information, please visit www.bristolgate.com.

For more information, please contact:

Michael Capombassis

President

416-921-7076 x 248

On September 16. 2021, Bristol Gate Canadian Equity portfolio manager Izet Elmazi discussed the differences in the Canadian equity market to the US Equity market, the importance of high active share and high quality, and how to best utilize the Canadian Equity strategy in portfolios.

Important Disclosures

There is a risk of loss inherent in any investment; past performance is not indicative of future results. Prospective and existing investors in Bristol Gate’s pooled funds or ETF funds should refer to the fund’s offering documents which outline the risk factors associated with a decision to invest. Separately managed account clients should refer to disclosure documents provided which outline risks of investing. Pursuant to SEC regulations, a description of risks associated with Bristol Gate’s strategies is also contained in Bristol Gate’s Form ADV Part 2A located at www.bristolgate.com/regulatory-documents.

This piece is presented for illustrative and discussion purposes only. It should not be considered as personal investment advice or an offer or solicitation to buy and/or sell securities and it does not consider unique objectives, constraints, or financial needs of the individual. Under no circumstances does this piece suggest that you should time the market in any way or make investment decisions based on the content. Investors are advised that their investments are not guaranteed, their values change frequently, and past performance may not be repeated. References to specific securities are presented to illustrate the application of our investment philosophy only, do not represent all of the securities purchased, sold or recommended for the portfolio, it should not be assumed that investments in the securities identified were or will be profitable and should not be considered recommendations by Bristol Gate Capital Partners Inc. A full list of security holdings is available upon request. For more information contact Bristol Gate Capital Partners Inc. directly. The information contained in this piece is the opinion of Bristol Gate Capital Partners Inc. and/or its employees as of the date of the piece and is subject to change without notice. Every effort has been made to ensure accuracy in this piece at the time of publication; however, accuracy cannot be guaranteed. Market conditions may change and Bristol Gate Capital Partners Inc. accepts no responsibility for individual investment decisions arising from the use of or reliance on the information contained herein. We strongly recommend you consult with a financial advisor prior to making any investment decisions. Please refer to the Legal section of Bristol Gate’s website for additional information at bristolgate.com.

A Note About Forward-Looking Statements

This report may contain forward-looking statements including, but not limited to, statements about the Bristol Gate strategies, risks, expected performance and condition. Forward-looking statements include statements that are predictive in nature, that depend upon or refer to future events and conditions or include words such as “may”, “could”, “would”, “should”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “estimate” and similar forward-looking expressions or negative versions thereof.

These forward-looking statements are subject to various risks, uncertainties and assumptions about the investment strategies, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. Readers are cautioned not to place undue reliance on forward-looking statements and consider the above-mentioned factors and other factors carefully before making any investment decisions. All opinions contained in forward-looking statements are subject to change without notice and are provided in good faith. Forward-looking statements are not guarantees of future performance, and actual results could differ materially from those expressed or implied in any forward-looking statements. Bristol Gate Capital Partners Inc. has no specific intention of updating any forward-looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation.

Takes 2 minutes

Takes 2 minutes